Individual Pension Plans

An Individual Pension Plan (IPP) provides the platform for individuals to maximize the accumulation of registered retirement assets and employers to take advantage of substantial corporate deductions. Our executive pension experts have helped thousands of employers, business owners, incorporated professionals, and key executives prepare for a successful retirement.

/ WHAT IS AN IPP

Individual Pension Plans are the most tax effective registered retirement arrangement permissible under tax legislation.

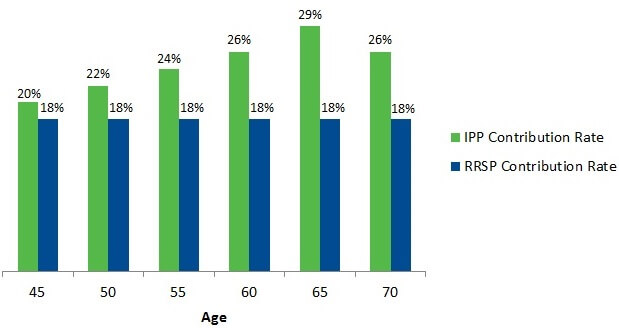

Ideally suited for business owners, incorporated professionals, and highly compensated employees, Individual Pension Plans (IPPs) allow for the tax-sheltering and accumulation of more registered assets through higher employer contributions than any other retirement vehicle available. Not only do IPPs generate fiscally sound retirement savings and income, they provide significant tax advantages for employers making contributions. In addition, unlike a Registered Retirement Savings Plan (RRSP), the contribution room available increases with age: the older the member, the higher the contribution room. This means that more company capital can be contributed tax-deductible and more funds being saved for retirement.

/ OUR EXPERIENCE

We take pride in our ability to provide careful and diligent service to clients across the country

President - Western Clinical Engineering Ltd.

❝Regardless of the outcome, I thought I would write to express my personal appreciation to you for your efforts that went above and beyond your normal duties, and for taking the time to talk with us.❞

Retired Executive EWOS Canada Ltd.

❝I want to thank you all for your excellent customer service which you have provided me over (especially) the past year. At a time of change from a large company to semi-retirement mode, your team has been most helpful and you have “old-school” traditional values. I hope you continue doing what you do above-average. You are all above-average and I highly commend you all. ❞

Request a Quote Now

Let our New Plans Team customize a complimentary plan funding quote just for you. Please click here to be directed to our Quote Request Form.

Not ready for a quote just yet? Already a client? Drop us a note below with any questions you have and we will get back to you shortly.